Setting the Price

Factors Influencing Pricing Decisions

Pricing decisions are influenced by a variety of factors, both internal and external, that organizations must consider to set effective and competitive prices. The following is an overview of the key factors affecting pricing decisions.

Internal Factors Affecting Price

Internal factors significantly influence pricing decisions and include considerations such as marketing objectives, marketing mix strategy, and cost structures. Below are the key internal factors that affect pricing.

Production Costs

Production costs are the costs associated with producing goods or delivering services, including both variable and fixed costs, and set the lower limit for pricing.

Variable costs are costs that change with production volume, such as raw materials and labor. Prices must be set above variable costs to ensure each sale contributes to covering fixed costs.

Fixed costs are stable expenses like rent and salaries that do not vary with production levels. Pricing strategies must account for recovering these costs over time.

Companies must ensure that prices cover these types of costs to achieve profitability.

Marketing Objectives

Pricing strategies must be aligned with an organization’s broader marketing objectives, such as maximizing current profit, increasing market share, or positioning as a premium brand.

Examples

Marketing Objectives

Survive the Recession: A company may set lower prices to maintain sales volume and cash flow during economic downturns.

Maximize Current Profit: Prices may be set at a level that maximizes immediate profits, often through premium pricing strategies.

Increase Market Share: Competitive pricing may be used to attract more customers and expand market presence.

Lead the Market in Quality: Higher prices can signal superior quality and establish a brand as a market leader.

Marketing Mix Strategy

Price must be coordinated with other elements of the marketing mix — including product features, distribution channels, and promotional strategies — to create a cohesive brand offering.

Examples

Marketing Mix Strategy

Product Design: The price should reflect the product’s design and quality. A premium product may justify a higher price point.

Distribution Channels: Pricing can vary depending on the distribution strategy. For example, exclusive distribution might support higher pricing.

Promotional Activities: Discounts or promotional pricing can be used to boost sales or introduce new products.

Product Lifecycle Stage

The stage of the product in its lifecycle (introduction, growth, maturity, and decline) can influence pricing strategies. For example, introductory pricing may be lower to attract early adopters.

External Factors Affecting Price

Several external factors can significantly influence pricing decisions for products and services. Here are the key external factors that affect pricing.

Market and Demand

The state of the market sets the upper limits for pricing. High demand can allow for higher prices, while low demand may require price reductions to attract buyers.

Price Elasticity of Demand

Price elasticity of demand is a measure of how sensitive consumers are to changes in price for a particular product. It tells us how much the demand for a product changes when its price changes.

Calculating Price Elasticity of Demand

Price elasticity of demand measures how the quantity demanded of a product changes in response to a change in its price. This is the ratio of the percentage change in the quantity demanded to the percentage change in price.

Types of Demand Elasticity

There are two types of demand elasticity a product can be:

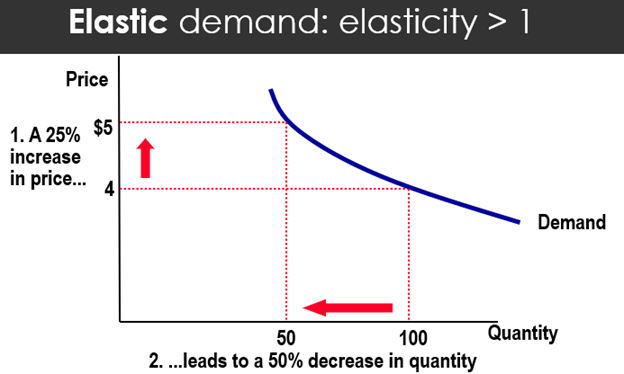

- Elastic Demand: If a small change in price leads to a large change in quantity demanded, the product is considered elastic. This typically occurs with non-essential or luxury items where substitutes are readily available (PED is greater than 1).

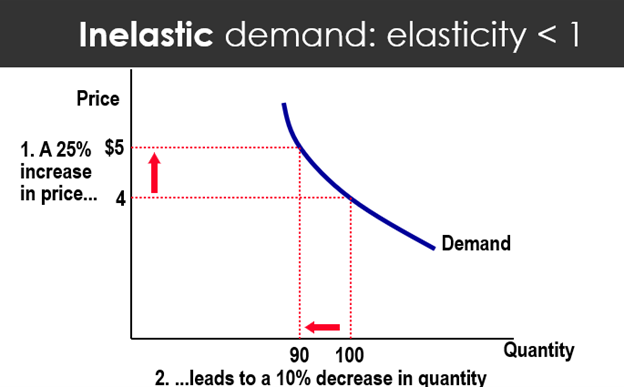

- Inelastic Demand: If a change in price leads to a small change in quantity demanded, the product is considered inelastic. This is common with essential goods that have fewer substitutes, like gasoline or prescription medications (PED is smaller than 1).

Factors Influencing Demand Elasticity

Certain factors influence demand elasticity including:

- Availability of Substitutes: Products with many alternatives tend to have more elastic demand.

- Necessity vs. Luxury: Essential items typically have more inelastic demand compared to luxury items.

- Time Frame: Demand often becomes more elastic over time as consumers can adjust their behavior.

- Proportion of Income: Items that consume a larger portion of income tend to have more elastic demand.

- Brand Loyalty: Strong brand loyalty can make demand more inelastic.

Examples

Price Elasticity of Demand

Consider a popular beach resort during peak summer season. Even if they raise their prices significantly, they might not see a big drop in bookings because people have limited alternatives (few substitutes) and are willing to pay more for their summer vacation. This would be an example of relatively inelastic demand.

Now, think about a budget airline offering flights to various destinations. If they slightly increase their prices, they might see a substantial decrease in bookings as price-sensitive travelers opt for competitors (many substitutes) or choose not to travel. This would be an example of elastic demand.

Consumer Perception of Price and Value

Consumers’ perception of a product’s value influences their willingness to pay. A higher perceived value can justify a higher price point.

Competitors’ Prices and Offers

The prices set by competitors can heavily influence a company’s pricing strategy. Businesses often adjust their prices to remain competitive, either by matching or differentiating from competitors’ prices.

Economic Environment

Economic conditions — such as inflation rates, unemployment levels, and consumer spending habits — impact pricing strategies. In economic downturns, consumers may become more price-sensitive, necessitating price adjustments.

Government Regulations

Laws and regulations, including taxes and tariffs, can affect production costs and pricing decisions. Compliance with legal requirements is essential when setting prices.

Media Attributions

- Figure 1: “Price elasticity of demand formula” by the author is under a CC BY-NC-SA 4.0 license.

- Figure 2: “Elastic demand” by the author is under a CC BY-NC-SA 4.0 license.

- Figure 3: “Inelastic demand” by the author is under a CC BY-NC-SA 4.0 license.

- Figure 4: “White Outdoor Lounge Chairs” by Colon Freld (2019), via Pexels, is used under the Pexels license.

- Figure 5: “Photograph of an Orange and White Airplane” by matt key (2020), via Pexels, is used under the Pexels license.

Costs that change with production volume, such as raw materials and labor. Prices must be set above these costs to ensure profitability.

Stable expenses like rent and salaries that do not vary with production levels. Pricing strategies must account for recovering these costs over time.

A measure of how sensitive consumers are to price changes. Elastic demand occurs when small price changes lead to significant changes in quantity demanded, while inelastic demand sees little change in demand despite price shifts.